Level 3 Management

The

developmental cycle is central to the Level 3 Management controversy. You only

really understand the project parameters after you are well into the investment.

With this, in typical applications, it is very difficult to anticipate the final

cost and schedule position and even the final configuration of the product. The

art of the possible will either be discovered or the quest becomes too expensive

and the project is cancelled. This is a normal aspect of Level 3 management. This

uncertainty becomes particularly arduous where developers are required to provide

a firm price a bid, as one would rightfully expect at Level 2. The

developmental cycle is central to the Level 3 Management controversy. You only

really understand the project parameters after you are well into the investment.

With this, in typical applications, it is very difficult to anticipate the final

cost and schedule position and even the final configuration of the product. The

art of the possible will either be discovered or the quest becomes too expensive

and the project is cancelled. This is a normal aspect of Level 3 management. This

uncertainty becomes particularly arduous where developers are required to provide

a firm price a bid, as one would rightfully expect at Level 2.

However the project becomes established, the key to success is rarely in any

of the formative documentation provided to Stakeholders as the basis for approval

to proceed. Rather, a "Project Leader", a senior officer above the station of

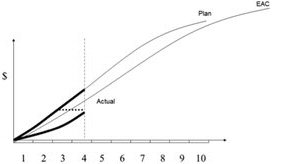

the Project Manager, oversees the trajectory of the estimate at complete. Trying

to establish a sense of "Earned Value",[1] attempts are made to see how the investment

is proving out. From this, an Estimate-At-Completion is calculated to guestimate

the final figures.

The Program

Manager can then reflect on the mission importance of the initiative and decide

whether the organization can afford to continue with it. Killing the project will,

obviously, save project costs but at the expense of foregoing the intended functional

outcome. Part of the judgment is realigning subcomponents, perhaps by eliminating

cost bearing functional components or by reducing technology to one that is tried

and proven technology. The Program

Manager can then reflect on the mission importance of the initiative and decide

whether the organization can afford to continue with it. Killing the project will,

obviously, save project costs but at the expense of foregoing the intended functional

outcome. Part of the judgment is realigning subcomponents, perhaps by eliminating

cost bearing functional components or by reducing technology to one that is tried

and proven technology.

An often understated, and easily discarded, dimension of intrigue in this regard

is the implication of relaxing requirements when nature "forces your hand." Keeping

sights trained on the end user's minimal requirements is also a key constraint

on how the project manager "plays the game."

Regarding Earned Value, the concept is good; the regime behind it is not so

good. Earned Value assessments in their initial incarnation entailed a detail

accounting exercise, the rigor of which was upset by the dynamic complexities.

Imagine highly detailed accounts, painstakingly compiled in a detail complexity

database, only to then be changed like sand on a beach with the first wave of

change. Successful Earned Value calculations require experience-based parametric

estimation.

When to Re-baseline

|

Learning quickly and getting this prediction correct as soon as possible can

make the difference between a viable outcome and a cancelled project. See Tao

Teh Ching quote.[2]

|

|

"Deal with things in their formative state... .

...before they grow confused"

-Tao Teh Ching

|

|

Deploying resources in pursuit of an unachievable outcome is a necessary casualty

of learning. Letting the problem fester unnaturally is a waste of opportunity

to take corrective action.

The analogy of baking a cake applies. Through the process of buying your ingredients,

mixing them, getting them into a pan and finally to the oven, the ability to change

trajectory — make a different shaped or a different flavored cake —

decreases exponentially as you progress through the process.

1. "Cost/Schedule Control Systems Criteria, The Management Guide to C/SCSC", Fleming, Quinten, Probus Publishing Company, 1988

2. "The Teachings of Immortals Chung and Lü", Shambhala Publications, 2000

|